Order-to-Cash (O2C) is the end-to-end business process that converts customer orders into cash through credit management, invoicing, collections, and payment reconciliation.

- Start: Customer order

- End: Payment applied and reconciled

- Goal: Reduce DSO and accelerate cash flow

It includes credit approval, invoicing, collections, cash application, and reconciliation steps that directly impact accounts receivable automation and revenue realization.

Order-to-Cash (O2C): Key Questions Answered

What is Order-to-Cash (O2C)?

O2C is the end-to-end process of converting customer orders into cash through invoicing, collections, and payment reconciliation.

Why is O2C important?

It directly impacts cash flow, Days Sales Outstanding (DSO), and working capital efficiency.

How does AI improve O2C?

AI automates credit, collections, and cash application to reduce delays, errors, and manual effort.

An optimized O2C process accelerates invoice-to-cash timelines, reduces revenue leakage, prevents blocked orders, and improves enterprise cash flow visibility.

What is Order to Cash (O2C) process cycle meaning?

The Order-to-Cash cycle begins when a customer order is received and ends when payment is applied and reconciled in the general ledger. It includes credit assessment, order fulfillment, invoicing, collections, cash application, and dispute resolution.

The goal is to accelerate revenue realization by reducing delays in invoicing, collections, and payment reconciliation.

Why the Order-to-Cash Process Matters in Accounts Receivable

The cash conversion process directly impacts cash flow by ensuring customer orders are fulfilled, invoiced, and reconciled efficiently. Faster payment collection improves liquidity, reduces Days Sales Outstanding (DSO), and enhances working capital visibility across finance operations.

Summary: A well-optimized O2C process improves liquidity, reduces delays, and enhances financial visibility.

This is a core part of order-to-cash cycle optimization.

Why Most O2C Initiatives Fail

- Disconnected ERP systems across business units

- Lack of real-time visibility into receivables

- Manual cash application and reconciliation

- Delayed dispute resolution processes

- Reactive collections instead of predictive strategies

Learn more about why DSO increases and how to reduce it to improve cash flow performance.

Result: Higher DSO, poor cash flow visibility, and revenue leakage.

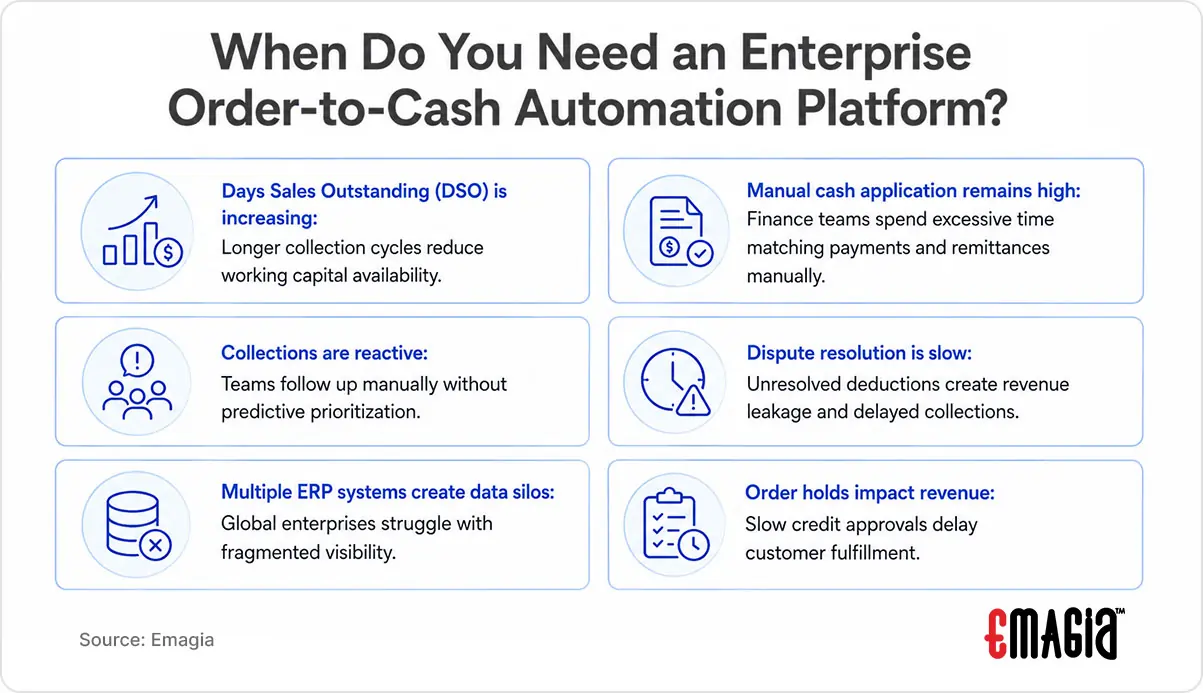

When Do You Need an Enterprise Order-to-Cash Automation Platform?

Not every organization needs a full enterprise order-to-cash automation platform immediately. However, when receivables complexity begins to impact working capital, customer experience, and finance productivity, automation becomes a strategic necessity.

Common indicators include:

- Days Sales Outstanding (DSO) is increasing: Longer collection cycles reduce working capital availability.

- Manual cash application remains high: Finance teams spend excessive time matching payments and remittances manually.

- Collections are reactive: Teams follow up manually without predictive prioritization.

- Dispute resolution is slow: Unresolved deductions create revenue leakage and delayed collections.

- Multiple ERP systems create data silos: Global enterprises struggle with fragmented visibility.

- Order holds impact revenue: Slow credit approvals delay customer fulfillment.

For enterprise finance organizations, these signals often indicate the need for a scalable order-to-cash automation platform that can unify workflows, improve visibility, and accelerate revenue realization.

Explore Solution →

Order-to-Cash as a Strategic CFO Lever

For enterprise CFOs, the invoice-to-cash cycle is more than an operational workflow. It is a strategic lever that influences liquidity, credit risk exposure, revenue predictability, and investor confidence.

High-performing finance organizations treat O2C as a data-driven revenue engine—using automation, AI, and predictive analytics to optimize every stage of the cycle.

Summary: O2C acts as a strategic lever for improving liquidity, reducing risk, and enhancing revenue predictability.

Customer Experience Impact of the O2C Process

Efficient Order-to-Cash workflows ensure accurate billing, timely order fulfillment, and transparent payment communication. This improves customer satisfaction and strengthens long-term customer relationships.

Expanding the Importance of End-to-End O2C Visibility

End-to-end visibility across the cash conversion process is critical for informed decision-making. Organizations with limited visibility often face delayed cash flows, untracked deductions, and disputes, which can impact both revenue and customer satisfaction. By consolidating data from all O2C touchpoints—order entry, invoicing, AR, collections, and cash application—businesses can gain real-time insight into the status of receivables and proactively address issues.

Modern O2C platforms integrate data from ERP systems, bank portals, and customer payment platforms, enabling comprehensive dashboards and reporting. This unified view not only improves operational efficiency but also supports predictive decision-making through AI-driven analytics.

Role of Technology in Modern O2C

Modern O2C platforms replace manual spreadsheets and fragmented ERP workflows with automation, analytics, and intelligent data capture. These technologies reduce errors, accelerate processing, and provide real-time insight into receivables performance.

Modern O2C platforms enhance forecasting accuracy, identify payment anomalies, and optimize collections strategies through data-driven automation. Intelligent document processing captures remittance data from emails, PDFs, and portals, reducing manual reconciliation effort.

Shorten the cash conversion process with Digital Invoicing & Payments. Read eBook

Enterprise Platform Capabilities Beyond Basic O2C Automation

Enterprise finance organizations require more than workflow automation. Modern order-to-cash platforms must support scalability, governance, integration, and enterprise-wide visibility across global finance operations.

- ERP and banking integrations: Native connectivity with SAP, Oracle, NetSuite, Microsoft Dynamics, payment gateways, and banking systems.

- AI copilots for finance teams: Intelligent assistants that help prioritize collections, surface anomalies, and support finance decision-making.

- Real-time executive analytics: Dashboards for DSO, CEI, dispute aging, forecasting, and enterprise receivables visibility.

- Global scalability: Support for multi-entity, multilingual, multi-currency, and region-specific finance operations.

- Workflow orchestration: Cross-functional automation spanning credit, collections, disputes, approvals, and exception management.

- Customer self-service portals: Digital access for invoices, payments, disputes, and communication workflows.

- Governance and compliance controls: Auditability, approval controls, role-based access, and regulatory alignment.

These enterprise capabilities differentiate scalable order-to-cash automation platforms from basic workflow tools.

What are the steps in the Order to Cash process

The steps in an Order to Cash process include customer order, credit management, fulfillment, billing/invoicing, payment and collections, cash application and ledger posting. Each step in the process impacts the latter stages in the process. For example, cash application impacts collections, and collections impact credit decisions and sales order acceptance.

Order-to-Cash Process Steps (7 Key Stages)

Process Flow Diagram")

End-to-end O2C workflow showing how AI connects credit, invoicing, collections, and cash application

- Customer Order: Order is received

- Credit Approval: Risk is evaluated

- Order Fulfillment: Goods/services delivered

- Invoicing: Invoice generated

- Collections: Payment follow-up

- Cash Application: Payment matched

- Dispute Resolution: Issues resolved

Credit:

The process often starts with a customer order, which initiates the credit process. The credit process involves gathering and analyzing information on the customer to determine their creditworthiness and to set the level of credit to extend to them. The data comes from the customer’s financials and other sources, including credit-rating agencies, trade groups, and internal records if the buyer is an existing customer.

Preventing Order Holds Through Credit Automation

Automated credit risk assessment enables faster approval of customer orders by evaluating financial exposure in real time. This prevents order holds and accelerates revenue realization across the Order-to-Cash cycle.

Modern Credit Risk Assessment

Modern credit management uses real-time data and analytics to assess customer risk, adjust credit limits, and prevent blocked orders.

Invoicing:

Upon order fulfillment, billing (consumers) or invoicing (businesses) must be done timely and accurately, through whatever delivery mechanism is necessary. These might include EDI, email, regular mail, fax or via portals. Timely invoicing is vital to timely payment. But accuracy is just as important. Invoices with incorrect or missing information slow down the payment process, creating confusion and additional work.

Electronic Invoicing and Compliance

Digital invoicing solutions reduce paper processing, standardize invoice formats, and ensure compliance with local and international regulations. By leveraging AI, invoice errors can be automatically detected and corrected before sending, reducing disputes and accelerating payment cycles. Integration with ERP and customer portals ensures seamless invoice delivery and visibility.

AR Portfolio Management:

The customer processes the invoice and pays it on time according to terms in a perfect world. Then the order-to-cash team applies the payment to the invoice or invoices, closing them out. The closed invoices relieve collections of further action and free sales to take additional orders. But the AR portfolio must be tracked and managed, with accurate and timely information provided to the collections department.

Advanced AR Monitoring and Analytics

Advanced AR management platforms monitor receivables in real time, identify overdue invoices, and prioritize high-risk accounts for early intervention.

Portfolio Segmentation and Optimization

Segmenting AR portfolios based on payment behavior, customer size, region, or product line enables more targeted collection strategies. AI-driven segmentation allows the system to suggest customized reminders, payment plans, or escalation workflows. Integration with dashboards provides executives with a real-time, enterprise-wide view of receivables health, supporting strategic decisions in cash management.

Collections:

Collections process departments follow up on open invoices to encourage and obtain payment. Collectors must have accurate and timely payment information, or they will waste time collecting on invoices already paid. Collectors employ emails, phone calls, and other tools in communicating with customers to collect money owed.

Automated Collections Workflow

Automated collections workflows send timely reminders and prioritize accounts based on payment behavior, improving collection effectiveness.

Customer Experience in Collections

Maintaining positive customer relationships during collections is essential. Modern O2C platforms offer self-service portals where customers can view their balances, submit payments, and resolve disputes without direct intervention. This reduces friction, improves satisfaction, and allows collectors to focus on more complex cases, ultimately supporting long-term revenue growth.

Cash Application:

Cash application is the reconciliation step of matching payments to invoices. Remittance information should accompany payments to indicate which invoice or invoices the customer is paying. Check payments include attached remittance information.

But with the shift to a variety of modern non-check payment formats, remittance information comes in separately, requiring an extra step. Remittance information now must be matched to payment before AR can apply the payment to open invoices and then record it in the company’s general ledger. Cash application in accounts receivable comes at the end of the process but feeds back essential information to collections, credit and sales.

AI-Enhanced Cash Matching

Automated cash application systems reconcile payments with invoices using intelligent matching logic, even when remittance details are incomplete.

Reducing Deductions and Disputes

Payments do not always match invoices. Customers may short-pay or dispute amounts due to errors or misunderstandings. Automated cash application platforms flag mismatches and route them to appropriate teams for resolution. AI can suggest resolutions based on historical patterns, helping finance teams reduce manual effort and cycle times. Timely resolution of deductions not only improves cash flow but also provides insights into upstream operational issues, such as invoicing errors or delivery discrepancies.

Dispute Management:

Dispute management is a critical component of the receivables workflow. Every short payment, missing invoice, or invoicing error must be investigated and resolved quickly to prevent revenue leakage. Effective dispute management relies on accurate data, streamlined workflows, and clear communication with customers.

Preventing Revenue Leakage Through Automation

Automated dispute workflows classify short-pays and deductions, route them to appropriate teams, and accelerate resolution.

Automated Dispute Resolution

AI tools analyze incoming disputes, classify them by type, and prioritize based on potential financial impact. Automated workflows route disputes to the right teams and provide recommended actions based on historical resolutions. This reduces resolution time and ensures that disputes are handled consistently across the enterprise.

Integration with cash conversion process

Dispute resolution is closely linked to credit, collections, and cash application. Insights gained from disputes can feed back into credit assessment policies, improve invoicing accuracy, and enhance collections strategies. By integrating dispute management within the overall O2C platform, businesses can close the loop on process inefficiencies and continuously improve performance.

Transforming Order-to-Cash with Emagia Global Deployment: The ConvaTec GBS Success Story. Watch Now

Business and Financial Impact of O2C Automation

Enterprise O2C automation delivers measurable financial impact by accelerating revenue realization, reducing operational costs, and improving working capital performance.

- Lower Days Sales Outstanding (DSO): Faster collections and automated payment matching improve cash conversion speed.

- Reduced manual processing costs: Automation decreases effort across collections, reconciliation, and dispute workflows.

- Improved cash flow visibility: Real-time dashboards provide finance leaders with better forecasting and liquidity insights.

- Reduced revenue leakage: Faster dispute resolution and more accurate invoicing minimize avoidable losses.

- Higher finance team productivity: Teams focus on strategic exception management instead of repetitive tasks.

- Stronger customer retention: Better billing accuracy and communication improve customer experience.

How AI Transforms the Order-to-Cash Process

AI acts as the digital backbone of the Order-to-Cash process, while finance teams focus on high-value strategy, exception handling, and customer relationships.

- AI-powered credit scoring reduces blocked orders

- Predictive collections lowers DSO

- Intelligent cash matching improves auto-application rates

- Automated dispute classification reduces resolution time

- Predictive analytics improves cash flow forecasting

Summary: AI-driven O2C improves speed, accuracy, and cash flow visibility across finance operations.

Human-in-the-loop approach: AI handles high-volume, repetitive tasks such as matching payments and prioritizing collections, while finance teams are alerted only when human judgment is required for complex exceptions or strategic decisions.

Want to automate your O2C process?

Estimate Your O2C Impact

If your company reduces DSO by just 5–10 days, the improvement in working capital can be significant.

Example: A $100M revenue company can unlock millions in cash flow.

Trusted by global enterprises to reduce DSO by up to 30%.

Reduce Your DSO in 90 Days → See How

ERP Integration in Order-to-Cash

Order-to-Cash systems integrate with ERP platforms to synchronize order fulfillment, invoicing, accounts receivable, and payment reconciliation. ERP-integrated O2C automation improves posting accuracy and reduces manual financial workflows.

Overcoming the Complexity in the Order to Cash Process

The invoice-to-cash cycle is inherently complex due to multiple interconnected steps, diverse data sources, and a variety of payment channels. For global enterprises, complexities multiply with multiple currencies, languages, and regional compliance requirements. Manual management of this complexity is not only time-consuming but prone to errors, leading to delayed cash flow, revenue leakage, and poor customer experience.

Challenges in Modern O2C Operations

- Multiple ERPs or accounting systems across business units

- High volume of transactions and exceptions

- Inconsistent customer data and incomplete remittance information

- Manual reconciliation and dispute resolution

- Fragmented visibility into cash positions across geographies

Enterprise Implementation Challenges in O2C Automation

While automation delivers significant operational gains, enterprise implementation often introduces its own complexity. Large finance organizations must address both technology and process transformation challenges.

- ERP integration complexity: Connecting multiple SAP, Oracle, or legacy systems across regions requires careful architecture planning.

- Poor master data quality: Inaccurate customer records, payment references, and account structures reduce automation effectiveness.

- Fragmented business processes: Different business units often follow inconsistent collections, dispute, and credit workflows.

- Incomplete remittance data: Unstructured payment information creates matching and reconciliation bottlenecks.

- Regional compliance requirements: Global enterprises must support local tax, invoicing, and financial regulations.

- Lack of executive sponsorship: Finance transformation initiatives stall without clear ownership and governance.

Successful enterprise O2C automation requires aligning technology implementation with process standardization, governance, and organizational adoption.

AI and Hyperautomation Solutions

Hyperautomation in Order-to-Cash combines workflow automation, intelligent data capture, and advanced analytics to streamline credit, invoicing, collections, cash application, and dispute resolution. By unifying these capabilities, enterprises reduce manual effort, improve accuracy, and gain real-time visibility across the entire cash conversion process.

Advanced Analytics for Cash Flow Forecasting

Analytics plays a critical role in understanding and optimizing the cash conversion process. Descriptive analytics provides insights into current performance, predictive analytics forecasts future cash flow trends, and prescriptive analytics recommends actionable steps to improve liquidity. With AI-enhanced analytics dashboards, finance teams can monitor KPIs like DSO, average payment times, and outstanding receivables across regions, business units, and customer segments.

Digital Assistants and Customer Interaction

AI-powered digital assistants improve both internal workflows and customer experience. For example, chatbots can interact with customers to answer invoice-related queries, provide payment options, and guide them through self-service portals. Internally, digital assistants alert finance teams to anomalies, prioritize critical tasks, and recommend interventions based on real-time data analysis.

Benefits of Automation and AI Integration

- Reduced operational errors and exceptions

- Faster invoice processing and cash application

- Proactive identification of credit risks and potential disputes

- Real-time visibility into receivables, payments, and disputes

- Enhanced customer satisfaction through timely communication and self-service options

- Data-driven decision making enabled by predictive and prescriptive analytics

Enterprise Use Cases

- Global Cash Visibility: Consolidates multi-entity receivables into a unified dashboard.

- Predictive Collections: Identifies high-risk accounts for proactive follow-up.

- Exception Handling: Automatically routes disputed or short-paid invoices for resolution.

- Customer Self-Service: Enables invoice access, payment tracking, and dispute management.

- Dynamic Credit Monitoring: Continuously adjusts credit exposure based on risk signals.

AI-Driven Insights for Finance Teams

AI does not simply automate tasks—it transforms decision-making. Finance teams can access real-time dashboards that show cash flow forecasts, overdue invoices, dispute trends, and high-risk accounts. With AI-powered insights, companies can identify bottlenecks, optimize collections strategies, and continuously refine their receivables workflows.

Integration With Other Enterprise Systems

Modern O2C platforms integrate with ERP systems, CRM solutions, payment gateways, and procurement platforms. This ensures seamless data flow across the enterprise, reduces manual reconciliations, and provides a single source of truth for financial operations. Integration also supports advanced GEO strategies, optimizing processes according to regional compliance, language, and currency requirements.

Future of Order-to-Cash: Eight Predictions. Watch Now

What are the 3 levels of O2C maturity?

- Manual: Spreadsheet-driven, high errors

- ERP-Based: Rule-based automation

- AI-Driven: Predictive, touchless processing

Manual vs ERP-Based vs AI-Driven O2C

| Factor | Manual O2C | ERP-Only | AI-Driven O2C |

|---|---|---|---|

| Credit Approvals | Manual review | Rule-based | Predictive AI scoring |

| Collections | Reactive | Scheduled reminders | Predictive prioritization |

| Cash Application | Manual matching | Basic rules | High auto-match rates |

| Visibility | Limited | Dashboard reporting | Real-time predictive analytics |

Benchmark Your O2C Maturity

| Stage | Characteristics | Business Impact |

|---|---|---|

| Manual | Spreadsheets, emails, manual reconciliation | High DSO, frequent errors |

| ERP-Based | Rule-based workflows, limited automation | Moderate efficiency, limited insights |

| AI-Driven | Predictive analytics, automation, real-time dashboards | Lower DSO, optimized cash flow |

When should you move to AI-driven O2C?

- DSO is consistently increasing

- Manual cash application exceeds 30%

- Multiple ERPs create data silos

- Collections are reactive instead of predictive

Best Practices to Optimize the Order-to-Cash Cycle

Optimizing the O2C cycle requires a combination of process improvements, automation, and analytics. Companies that implement these best practices experience reduced DSO, improved cash flow, and enhanced customer satisfaction.

1. Automate Order Processing

- Reduce manual data entry through AI-enabled order validation

- Ensure orders are processed quickly and accurately across channels

- Integrate with ERP and CRM systems for seamless data flow

2. Implement AI-Based Credit Scoring

- Use predictive analytics to assess customer credit risk in real-time

- Set dynamic credit limits based on payment history and behavioral patterns

- Monitor credit exposure continuously across regions and portfolios

3. Optimize Invoice Management

- Adopt electronic invoicing (e-invoicing) for faster processing and compliance

- Standardize invoice formats to reduce errors and disputes

- Use AI to detect anomalies in invoice data before sending

4. Improve Payment Collection Strategies

- Offer multiple payment options to customers, including digital wallets and automated clearing

- Automate payment reminders and escalation for overdue accounts

- Leverage predictive analytics to prioritize high-risk collections

5. Enhance Dispute Resolution

- Implement AI-driven dispute tracking and categorization

- Resolve claims quickly to maintain customer trust

- Use insights from disputes to identify upstream process issues

6. Utilize Data Analytics for Decision-Making

- Monitor key KPIs such as Days Sales Outstanding (DSO), overdue invoices, and cash conversion cycles

- Apply predictive models to forecast cash flow and identify potential delays

- Leverage prescriptive analytics for actionable recommendations to improve financial performance

Summary: Applying automation and analytics in O2C reduces DSO and improves working capital efficiency.

O2C Metrics and KPIs to Track

Measuring performance is critical to continuous improvement. Key metrics include:

- DSO (Days Sales Outstanding): Average time to collect payment after invoice issuance

- Invoice Accuracy Rate: Percentage of invoices processed without errors

- Collection Effectiveness Index (CEI): Measures collection success against targets

- Dispute Resolution Time: Average time to resolve customer disputes

- Cash Application Accuracy: Percentage of payments applied correctly to invoices

- Customer Satisfaction Score: Tracks experience during the receivables workflow

Emerging Trends in Order-to-Cash

The O2C landscape is evolving rapidly with AI, automation, and advanced analytics. Current and emerging trends include:

- Predictive Cash Flow Analytics: Advanced analytics forecast receivables to improve liquidity planning and working capital management.

- Intelligent Exception Management: Automated identification and routing of anomalies in orders, invoices, and payments.

- Customer Self-Service Portals: Empowering customers to access invoices, submit payments, and resolve disputes independently.

- AI-Driven Process Optimization: Machine learning enhances credit, collections, and cash application workflows over time.

- Real-Time Dashboards: Live KPI visibility enables faster, data-driven decision-making across finance operations.

Transitioning from ERP-Based to AI-Powered O2C

Many enterprises rely on ERP systems for financial operations but struggle with limited automation, delayed insights, and manual reconciliation. Transitioning to an AI-powered O2C model enables real-time decision-making, predictive analytics, and touchless processing.

- Step 1: Identify manual bottlenecks in credit, collections, and cash application

- Step 2: Integrate AI layers with existing ERP systems

- Step 3: Automate high-volume workflows while maintaining human oversight

- Step 4: Use predictive analytics to optimize collections and cash flow

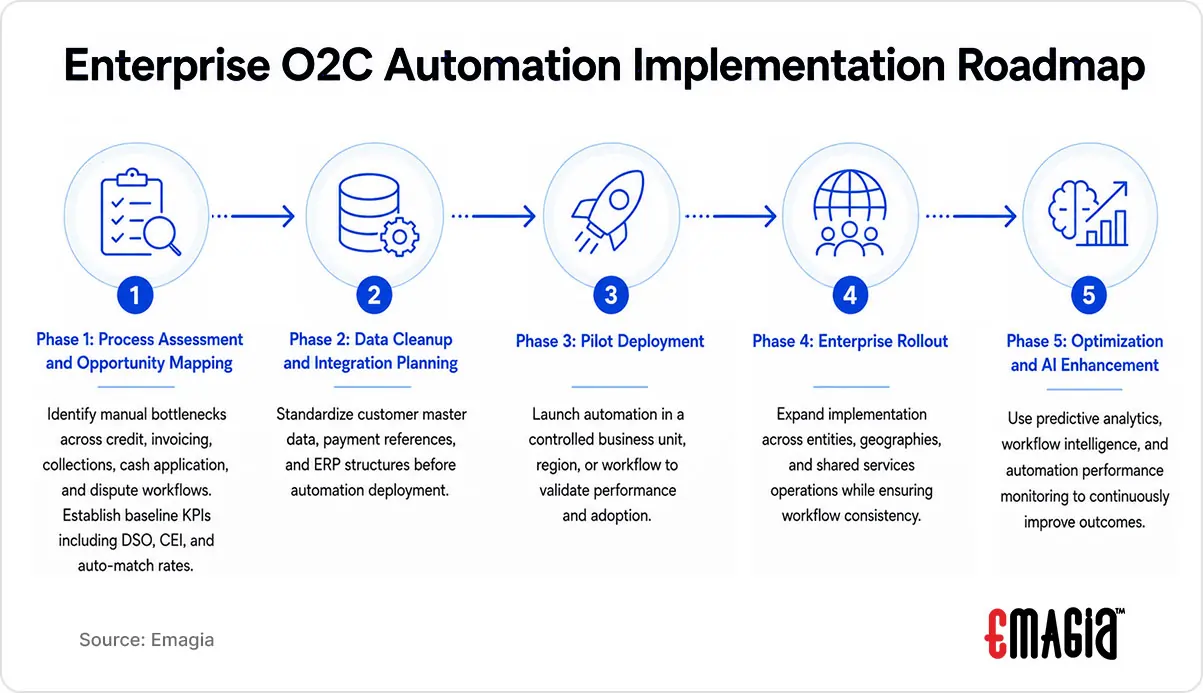

Enterprise O2C Automation Implementation Roadmap

Successful implementation of an enterprise order-to-cash automation platform requires a phased rollout approach rather than a full-scale transformation at once.

Phase 1: Process Assessment and Opportunity Mapping

Identify manual bottlenecks across credit, invoicing, collections, cash application, and dispute workflows. Establish baseline KPIs including DSO, CEI, and auto-match rates.

Phase 2: Data Cleanup and Integration Planning

Standardize customer master data, payment references, and ERP structures before automation deployment.

Phase 3: Pilot Deployment

Launch automation in a controlled business unit, region, or workflow to validate performance and adoption.

Phase 4: Enterprise Rollout

Expand implementation across entities, geographies, and shared services operations while ensuring workflow consistency.

Phase 5: Optimization and AI Enhancement

Use predictive analytics, workflow intelligence, and automation performance monitoring to continuously improve outcomes.

Why Change Management Determines O2C Success

Technology alone does not guarantee transformation success. Finance teams, collectors, shared services groups, and credit teams must adapt to new workflows and decision models.

- Redefining collector workflows and exception handling

- Aligning shared services processes globally

- Creating governance ownership across finance leadership

- Establishing KPI accountability and reporting standards

- Training teams to work alongside AI-driven workflows

Organizations that underestimate change management often struggle to realize expected ROI from O2C automation investments.

Why AI-Driven O2C Platforms Outperform Traditional Systems

- Real-time decision-making vs static ERP rules

- Predictive collections vs reactive follow-ups

- Touchless cash application vs manual matching

- Unified data vs siloed systems

How to Evaluate an Enterprise Order-to-Cash Automation Platform

Selecting the right order-to-cash automation platform requires evaluating more than feature lists. Enterprise finance teams should assess scalability, integration readiness, automation depth, and implementation support.

- ERP compatibility: Does the platform integrate with your existing ERP environment?

- Automation breadth: Does it cover credit, invoicing, collections, disputes, and cash application?

- AI maturity: Does the platform deliver predictive automation or only rule-based workflows?

- Implementation support: Is enterprise deployment assistance included?

- Analytics visibility: Are executive dashboards and performance insights available?

- Global scalability: Can the platform support multilingual, multi-entity, and regional finance operations?

- Security and compliance: Does it align with enterprise governance standards?

Questions CFOs Should Ask Before Selecting an O2C Automation Platform

- How long does enterprise implementation typically take?

- What ERP integrations are available out of the box?

- How much manual intervention is still required after deployment?

- What cash application auto-match rates are achievable?

- How does the platform support dispute automation?

- Can collections workflows be customized by geography or customer segment?

- What analytics and forecasting capabilities are included?

How Emagia Helps with Order-to-Cash Optimization

Emagia provides a unified, AI-driven O2C platform designed to address the complexity of modern finance operations. By combining automation, predictive analytics, and intelligent workflows, Emagia helps enterprises optimize every stage of the invoice-to-cash cycle.

Platform Capabilities

- AI-Powered Credit Management: Automates credit scoring, monitors risk, and adjusts limits dynamically

- Digital Order Processing: Validates orders, ensures compliance, and integrates with ERP/CRM systems

- Automated Invoicing and Payment Application: Generates accurate invoices, reconciles payments, and reduces manual effort

- Predictive Cash Flow Analytics: Forecasts receivables and provides actionable insights for liquidity management

- Dispute Resolution Management: Tracks, categorizes, and resolves disputes efficiently using AI-driven recommendations

Business Value and Enterprise Use Cases

- Global Enterprises: Consolidates O2C data across regions and currencies for a unified view of cash flow

- Collections Optimization: Prioritizes accounts based on AI-predicted payment behavior

- Credit Risk Management: Real-time monitoring and automatic adjustments to credit exposure

- Customer Experience: Digital portals and AI assistants reduce response times and enhance satisfaction

- Operational Efficiency: Automates repetitive tasks, enabling finance teams to focus on strategic decision-making

By leveraging Emagia’s intelligent O2C platform, companies can streamline operations, reduce DSO, and improve cash flow while providing a superior customer experience.

Order-to-Cash (O2C) Process FAQs

1. What is the Order-to-Cash (O2C) process?

O2C is the process from customer order to payment reconciliation that improves cash flow and reduces DSO.

2. Why is an efficient O2C process important for businesses?

Efficient O2C improves cash flow by accelerating invoicing, collections, and payment reconciliation.

3. What are the main steps in the Order-to-Cash cycle?

The O2C cycle includes order, credit, fulfillment, invoicing, collections, and payment reconciliation.

4. How does O2C automation reduce Days Sales Outstanding (DSO)?

O2C automation reduces DSO by accelerating invoice matching, credit approvals, and payment reconciliation.

5. How does automation in O2C prevent blocked customer orders?

AI-powered credit risk monitoring evaluates customer financial exposure in real time and enables faster approval of customer orders. This prevents order holds and accelerates revenue realization across the invoice-to-cash cycle.

6. How does ERP integration improve the receivables workflow?

ERP-integrated O2C platforms synchronize order fulfillment, invoicing, accounts receivable, and payment reconciliation. This improves posting accuracy, reduces manual financial workflows, and enhances real-time cash visibility.

7. How does O2C automation improve customer experience?

Efficient O2C workflows ensure accurate billing, timely order fulfillment, and transparent payment communication. This improves customer satisfaction and strengthens long-term customer relationships.

8. How does O2C automation prevent revenue leakage?

Automated dispute resolution enables faster investigation and settlement of short-pays and deductions. This prevents revenue leakage and improves the overall invoice-to-cash conversion cycle.

9. How does O2C automation improve working capital?

Automated reconciliation accelerates payment matching and posting, enabling finance teams to optimize liquidity and manage working capital more effectively across the revenue cycle.

10. What KPIs measure Order-to-Cash performance?

Key O2C KPIs include Days Sales Outstanding (DSO), Collection Effectiveness Index (CEI), invoice accuracy rate, dispute resolution time, cash application accuracy, and cash conversion cycle.

11. How long does enterprise O2C automation implementation take?

Implementation timelines vary based on ERP complexity, business units, and rollout scope. Enterprise deployments often begin with pilot implementations before expanding globally.

12. What should enterprises look for in an order-to-cash automation platform?

Key evaluation criteria include ERP integration, automation breadth, AI capabilities, analytics visibility, global scalability, dispute management, and implementation support.

13. What are the biggest O2C implementation challenges?

Common challenges include ERP integration complexity, poor master data quality, fragmented workflows, regional compliance requirements, and insufficient change management.