Order-to-cash (O2C) automation is the use of artificial intelligence (AI), robotic process automation (RPA), machine learning, and advanced analytics to automate the end-to-end receivables lifecycle—from order validation and credit approval to invoicing, collections, cash application, dispute resolution, and reconciliation.

For enterprise CFOs, O2C automation improves working capital performance by reducing Days Sales Outstanding (DSO), accelerating cash conversion, minimizing manual exceptions, and improving customer experience across global finance operations.

Key Business Outcomes of O2C Automation

- Reduce DSO by 30% or more

- Achieve 85%+ autonomous cash application match rates

- Accelerate credit decisions from days to minutes

- Lower receivables operating costs by 40%

- Improve real-time visibility across global AR operations

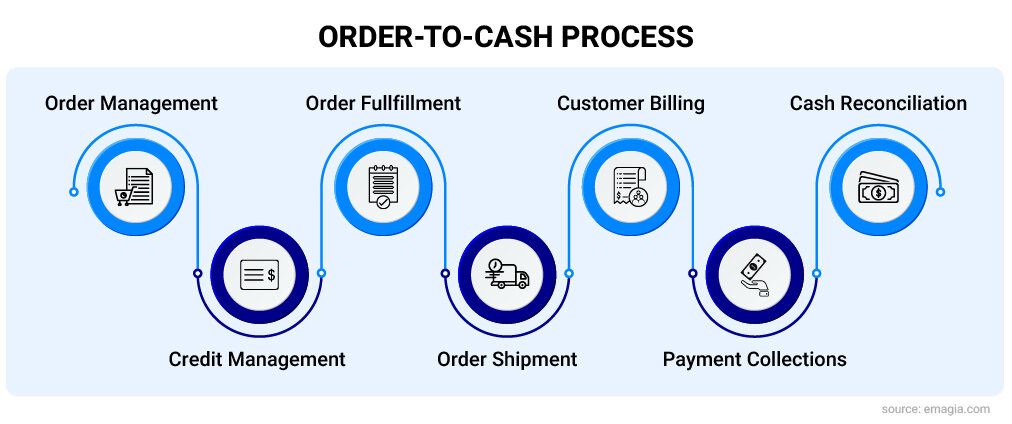

What Does Order-to-Cash Automation Include?

Enterprise O2C automation orchestrates the full receivables lifecycle across:

- Order capture and validation

- Credit risk assessment

- Invoice generation and delivery

- Collections workflow automation

- Cash application and remittance matching

- Dispute and deduction resolution

- AR reconciliation and reporting

This creates a unified finance operations layer across ERP, CRM, banking, and payment ecosystems.

How Order-to-Cash Automation Works

- Capture and validate customer orders

- Assess credit risk automatically

- Generate and deliver invoices

- Match incoming payments automatically

- Resolve deductions and disputes

- Reconcile receivables in real time

Integrated O2C Automation Replaces Automated AR

Enterprise finance leaders are shifting from isolated accounts receivable automation toward integrated, autonomous order-to-cash platforms that combine workflow orchestration, AI, analytics, and real-time receivables intelligence.

Manual O2C vs Basic AR Automation vs Autonomous O2C

| Capability | Manual O2C | Basic AR Automation | Autonomous O2C (Emagia) |

|---|---|---|---|

| Cash Application | Manual matching | Rule-based automation | AI autonomous matching |

| Exception Resolution | Human intervention | Limited workflows | Agentic AI reasoning |

| Multi-ERP Data Integration | Siloed | Partial | Cross-instance normalization |

| Remittance Processing | Manual extraction | Template dependent | Unstructured AI interpretation |

| Customer Self-Service | Manual support | Portal only | AI digital assistant |

See how autonomous O2C compares in real enterprise finance environments.

How Modern Enterprise O2C Architecture Works

Modern enterprise order-to-cash platforms unify structured and unstructured receivables data from ERP systems, customer communications, payment networks, and banking channels into a centralized finance intelligence layer.

This includes data from SAP, Oracle, NetSuite, Microsoft Dynamics, CRM systems, ACH payment files, SWIFT remittances, bank lockboxes, supplier networks, and customer portals.

By consolidating fragmented receivables data, enterprises can orchestrate credit, invoicing, collections, deductions, cash application, and reconciliation workflows in real time across global business units.

This architecture improves visibility, reduces manual handoffs, accelerates exception resolution, and enables better customer experiences through faster, more accurate receivables operations.

Challenges of Enterprise Order-to-Cash Automation

Enterprise order-to-cash automation is challenging because receivables data is fragmented across multiple systems, formats, and business units.

Large organizations often operate multiple ERP environments such as SAP, Oracle, NetSuite, Microsoft Dynamics, and legacy finance systems.

Enterprise-grade O2C automation requires cross-instance finance data normalization and unified visibility across structured and unstructured receivables data.

Transforming Order-to-Cash with Emagia Global Deployment: The ConvaTec GBS Success Story. Watch Now

AI Agents vs Traditional RPA in O2C Automation

Traditional robotic process automation (RPA) automates repetitive rule-based tasks but struggles when data is incomplete, inconsistent, or unstructured.

AI agents go further by reasoning through exceptions, interpreting remittance advice, predicting disputes, and autonomously recommending next actions.

For example, Emagia’s Gia AI assistant can help automate:

- Unstructured remittance interpretation

- Cash application exception resolution

- Collections prioritization

- Deduction workflow routing

- Customer self-service payment interactions

A Change in Human Involvement

Comprehensive, integrated automation markedly reduces the requirement for human involvement in traditional “work” such as repetitive information gathering, organizing, and reporting. Instead, humans can move to problem-solving and higher-order tasks.

Benefits of Overcoming O2C Automation Challenges

Integrated and hyper automated O2C platforms demonstrate such results as:

Integrated and hyper automated O2C platforms demonstrate such results as:

- Credit decisions in minutes and seconds rather than days or weeks

- Current AR of 85 percent or better

- Deduction processing in less than a week

- 85 percent or higher cash auto match

- Insights through visualizations and reporting

- 30+ percent reduction in DSO

- 40+ percent reduction in operations cost

- Customers experience high touch, high accuracy, and 24 X 7 X 365 digital assistance

Advanced automation technology provides cash forecasting and improves cash flow to support working capital management. With a stronger cash position and better forecasting, CFOs can manage debt, invest in product development, and finance initiatives.

From Process to Insight and Strategy

True O2C automation is here. The outcomes of an integrated and automated O2C process indicate the overall direction of finance work in general, which is away from managing process toward monitoring process, providing insights, and business strategizing. In addition, reporting will shift to real time, eventually eliminating the close processes. And efficiency gains will enable finance to shift its focus to the demands of enhanced customer experience and creating strategies for growth.

For more on how Emagia’s O2C Automation Platform can move your enterprise forward, Request an Enterprise O2C Assessment.

What Enterprise O2C Platforms Must Deliver

- Autonomous cash application

- AI-powered collections prioritization

- Dispute and deduction automation

- Predictive cash forecasting

- Global multi-currency receivables support

- ERP and CRM integrations

- Real-time CFO dashboards

- Customer-facing AI assistants

Frequently Asked Questions (FAQs) about Order to Cash Automation

What is order to cash automation?

Order-to-cash automation uses AI, workflow automation, and analytics to automate receivables workflows from order processing through payment reconciliation, reducing manual work, improving cash flow, and accelerating collections.

Why is order to cash process automation important?

Order to cash process automation increases efficiency, shortens cycle times, reduces Days Sales Outstanding (DSO), improves working capital, and enhances the customer experience by minimizing manual tasks and enabling real-time insights.

What are the main steps in the order to cash process?

The O2C process includes order capture, credit approval, invoicing, payment collection, cash application, dispute management, and reconciliation.

What are the benefits of using order to cash software?

Order to cash software delivers faster cash collection, improved AR accuracy, automated exception handling, actionable analytics, reduced operational costs, and enhanced customer satisfaction.

Can O2C automation software integrate with existing ERP and CRM systems?

Yes. Modern O2C automation platforms integrate seamlessly with ERP, CRM, banking systems, and other enterprise applications, enabling a single, unified view of receivables and cash flow across the organization.

How does AI improve the order to cash process?

AI enhances O2C automation by automating cash application, predicting and resolving exceptions, extracting remittance data from multiple formats, and providing insights for better decision-making, reducing manual intervention significantly.

What is the role of RPA in order to cash automation?

Robotic Process Automation (RPA) automates repetitive, rule-based tasks such as invoice processing, data entry, and payment reconciliation, freeing staff to focus on exception handling and strategic activities.

What are common challenges in the O2C cycle?

Challenges include fragmented ERP systems, inconsistent data sources, delayed cash application, manual deduction and dispute management, cross-currency complexities, and lack of real-time visibility. Integrated O2C platforms solve these challenges through automation and AI.

How does order to cash automation impact working capital?

By speeding up cash collection, improving AR accuracy, and reducing DSO, O2C automation increases available cash, strengthens liquidity, and allows CFOs to reinvest in strategic initiatives.

What makes Emagia a leading order to cash automation solution?

Emagia combines AI-powered cash application, workflow automation, analytics, and ERP integrations to help enterprise finance teams accelerate collections and improve receivables visibility.

Can order to cash automation handle multi-currency and global operations?

Yes. Advanced O2C automation platforms manage multi-currency transactions, global receivables, and international remittance formats, ensuring consistent and efficient cash collection across regions.

What is the difference between invoice to cash and order to cash automation?

Invoice to cash focuses primarily on invoicing, payment receipt, and cash application. Order to cash automation encompasses the entire sales-to-cash process, including order capture, credit management, fulfillment, invoicing, payment, cash application, and reconciliation.

How can businesses measure the success of O2C automation?

Key metrics include reduction in DSO, percentage of automated cash application, dispute and deduction resolution time, operational cost savings, AR accuracy, and improved customer satisfaction.