For most companies, today’s economy has depressed revenue and increased credit risk. On one hand, you need to increase sales by any means possible, including finding new customers and accepting higher credit risk. On the other hand, you need to control bad debt loss and the cash shortages resulting from financially weak, slow paying customers. Continue reading this article to learn more about building effective digital B2B credit process to drive more revenue and reduce risk.

What can a company do to resolve these conflicting imperatives?

One part of the solution is to maximize sales to new customers who have “reasonable” financial strength and a “tolerable” credit risk. Your company must define these terms consistent with its trade credit strategy (amended for the pandemic economy as appropriate). How desperate is the need for revenue? How much risk of slow and non-payment will you bear?

The amount of bad debt risk to be accepted is influenced heavily by the gross margin on sales. If the gross margin is high, the bad debt loss on some new accounts will be exceeded by the incremental profits earned on other new accounts who pay. If gross margin is low, it will require a high volume of revenue from new accounts to compensate for even a few customer defaults.

However, your competition will also seek to acquire new customers. How can you successfully compete? The answer is driving digital transformation in finance.

Create a Competitive Advantage

One competitive advantage is fast onboarding of customers and commencement of trading. Doing business with a new customer will, in many cases, pre-empt your competition from selling to that same customer. Companies seldom onboard multiple suppliers of the same product simultaneously. How fast is fast? Hackett’s World Class performance is two (2) days.

Once a company has agreed to buy from you, the first step in onboarding is to determine if you can extend credit to them, and if so, how much. Customers expect quick approval. Delay in credit approval and establishing an account gets the relationship off to a bad start, and may even induce the potential customer to reconsider doing business with you. However, a hasty and bad credit decision can result in seriously delayed payments and substantial credit losses.

What is the Solution to Improve the B2B Credit Process?

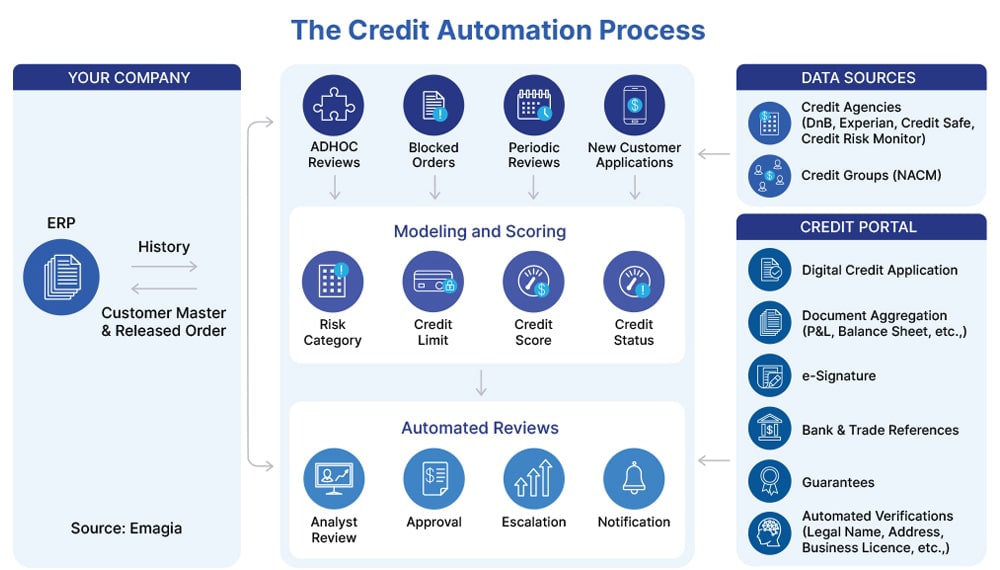

The best and right solution for these problems is establishing a digital credit process in your customer financial services that is powered by artificial intelligence.

- An digital credit application with digital signature completed and submitted by the prospective new customer

- Automated, real time links to credit bureau reports

- Digital credit scoring and digital credit decisioning

- AI-driven credit worthiness and credit limit recommendation

- A workflow for approvals of credit limit routing through your company’s delegation of authority matrix

- An AI-powered digital credit assistant to perform many of the credit vetting tasks, thereby dramatically reducing the manual effort

These capabilities will enable you to make a quality, fact-based credit limit decision in one to two business days and beat your competition, enhancing the success of your “new customer” sales effort. It will also decrease the manual credit management tasks by 70 – 80% and enable you to process a much higher volume of credit applications.

Clearly, an Artificial Intelligence (AI) Powered digital credit strategy can be a competitive advantage and help you boost your revenue.