Top line, bottom line, and cash flow – the three critical components in business – are the barometers of the health of a business, that influence its sustenance and growth. Order To Cash (OTC) is one business process that impacts all these three elements. While all of them are critical for businesses, cash flow has a definite edge over others because it is more real than the others. OTC, the main cash flow driver, has many subsets within it, and credit management is more important than it looks on the surface.

Onboarding customers or processing sales order without checking and ensuring their creditworthiness is risky. The top line and bottom line will be positively impacted when a sales order is received and fulfilled, but your business is at risk till you collect cash against the invoice. This calls for a robust credit management system in place. However, a cumbersome and time-consuming credit control process will drive away your existing customers and as well prospects if you are not a monopoly in your particular segment and/or region. To grow and scale profitably in a competitive environment, you need to address this dilemma of balancing the need for credit management and doing it without compromising on a seamless experience for your customers.

What is B2B Credit Automation For The Digital Era?

Working capital management of every company involves credit extended to their customers and credit availed from the vendors. Granting credit is an important tool for attracting and retaining customers. However, it is crucial for businesses to perform a credit check on the customers before extending credit, to avoid loss of revenue by way of bad debts. Till a few years back, most businesses except large enterprises were dependent on manual, paper-based processes in most activities in the business, including credit management. Many SME companies started tasting the benefits of technology with the emergence of small-to-midsize ERP systems, which have been performing the basic credit operations for businesses, among others.

However, today these systems are not enough because of the changing demands and expectations of individual and corporate customers. Most stand-alone ERP systems, even today, cannot complete credit approvals without inputting data collected manually from various sources. Most ERPs can automate only a small portion of credit control operations. This has opened up opportunities for niche add-on OTC applications that perform credit management including the credit control process intensively in its entirety with the minimum, if not nil, manual intervention. These new tools have made credit control easy and less risky for your business and your customers.

In today’s digital environment, customers expect a quick credit approval process to avoid spending non-productive time and effort on mundane tasks such as providing a lot of information by filling up paper applications for manual verification and approval. To meet the customer expectations and continue to be in business, businesses need to consider technology adoption in OTC processes including credit operations, to automate the following steps to make credit control autonomous.

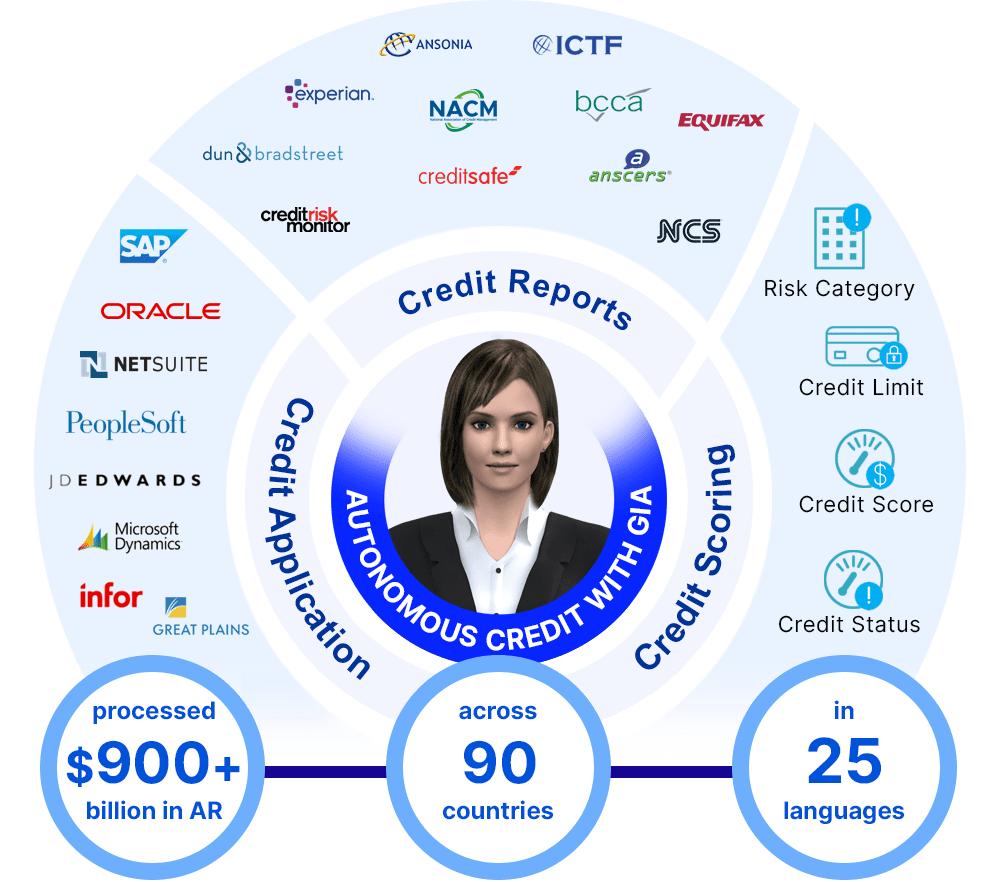

- Online credit application makes the application process simple and quicker for the customer.

- Digital signature in place of a manual signature on a paper application.

- Online reference check to avoid the manual process of sending paper applications to referenced parties and banks.

- Digital integration with external credit agencies, which is one of the top elements in the credit control process, is meant to collect credit information from third-party agencies.

- Automated credit to calculate a credit score based on the customer history, customer behavior, agency scores, and other factors.

- Rules-based credit limit granting classifies customers into various pre-defined buckets based on scores, rules, and other relevant parameters to help the approval process.

- Automated workflow approval minimizes the time and error in the credit approval process.

- Automatic periodic portfolio analysis to ensure that the credit worthiness of the new customer is confirmed before onboarding.

- Analytics and dashboards allow stakeholders in different functions and at various levels in an organization to get the required information in the proper format.

- Digital document storage to maintain a large volume of data in digital format rather than in hard copy formats to make data access easy and minimize storage space.

Why B2B Credit Automation is Critical For Digital Businesses?

While credit is nil or minimal in the B2C digital business space, it is as usual in the B2B digital business. Typical B2B digital businesses include cloud service, SaaS, PaaS, IaaS, XaaS providers, and B2B marketplaces. Like in conventional business models, it is an accepted business practice to extend credit to customers in digital businesses. Whether small or large, it is unavoidable for companies in digital business to have automated credit management in place.

The customer expectations from companies in digital business are even higher than conventional business because their business models are driven by digital technology. In digital business, the entire process from marketing to customer acquisition, onboarding, invoicing, and collection is integrated and online. The credit approvals have to be quicker and simple for the customers to continue engaging with your company and credit automation is a prerequisite to meet these expectations.

How AI is Enabling Autonomous Credit for Digital Businesses?

Automated credit applications are no longer acceptable in the digital transformation initiatives of businesses including digital businesses. Autonomous tools and applications are what businesses are now looking for in their strive to scale and be profitable. Emerging Industry 4.0 technologies like artificial intelligence (AI), machine learning (ML), deep learning (DL), robotics process automation (RPA), Big Data, and Blockchain, are among technologies that are leveraged to create autonomous processes like OTC that includes credit control management.

AI is arguably the most used technology in solutions that are designed to transform the way businesses manage and control credit. AI typically automates repetitive tasks and collects and analyzes large data sets to understand customer payment trends, make decisions, and learn customer behavior over time. AI shouldn’t be confused with robotic process automation (RPA); while RPA replicates simple, routine tasks, AI takes it to the next level of intelligent automation to transform the process autonomously.

Let us examine how AI-enabled credit solutions can help businesses achieve better customer experience, enhance the top line, improve the bottom line, and above all become more cash-efficient.

More Digital and Autonomous

A credit management solution enabled by AI minimizes, if not eliminates, the manual processing of routine, mundane, and low-value tasks that take away a lot of quality time of the credit team. Autonomous credit application automates the entire credit management process starting from credit application to credit approval, collection, application of cash, to reconciliation. It customizes the workflows for each customer based on each one’s profiling and behavior. Furthermore, it informs and alerts the credit professionals if credit is to be approved or not, when action is required, or when a change in the payment behavior of a customer happens.

Improved Data-Driven Processes

AI-driven credit solutions provide everyone concerned with the credit process in the organization with a wider and more transparent view of the customer credit. It collects credit information from various sources like credit agencies, banks, insurers, ERP, etc., and updates the data instantly, to provide credit professionals a real-time view of debt and collections. You have all credit data in one place, eliminating the need to maintain disparate systems or spreadsheets – a major reason hitherto for presenting differing data to different stakeholders. It helps managers to track the KPI of the credit team on the collection and debt collection efficiency. Tasks like the application of cash collected from customers and bank reconciliations can be completed in a few minutes with an AI-enabled credit solution, compared to the cumbersome and time-consuming manual process.

Makes it More Intelligent

Achieving cash targets is arguably the top KPI of credit professionals. AI-driven autonomous credit management solutions typically analyze historical data and customer payment behaviors to enable credit professionals to forecast cash flow more accurately and focus on customers whose behavior looks uncertain, more vigorously. AI-enabled credit tools simplify the credit processes, eliminate the possibilities for errors, and speed up the process cycle times. An autonomous credit application frees up credit professionals to spend more time on value tasks such as data analysis and customer management to enable make informed decisions.

Bottom Line

Credit management is a fundamental process in all companies including digital businesses. Businesses that have embraced digital transformation to create an autonomous credit management function benefit from better cash flow, less debt, lower finance costs, and enhanced profitability. You inevitably engage with a solutions provider that understands how credit management works in an organization and has proven the capability of their AI-powered credit solutions in achieving the expected results from an autonomous credit process.