What is a Bank Reconciliation Definition?

You take a bank statement, generally at the end of each month, from the bank. The cash and other deposits made to the company’s checking account are listed item by item in the statement. The statement also includes bank charges for account servicing costs.

Bank reconciliation is to verify your bookkeeping by looking at your bank statements and business accounts. Corporations use bank reconciliations to find any mistakes that may impact their financial reporting. It is also very crucial to prevent fraud that may occur.

The Purposes for Bank Reconciliation include:

- Fixing any errors

- Find and prevent fraud

- Have a better picture of the financial performance of the business

- It prepares you for filing taxes

Bank reconciliations should occur once a month and at the end of the month. Banks deliver the monthly statements at the end of each month which serves as a basis for reconciliation.

Unfinished bank reconciliations can lead to a few risks including cash shortfalls and bounced checks.

Lockbox and Remittance Data Extraction with AI. Read eBook

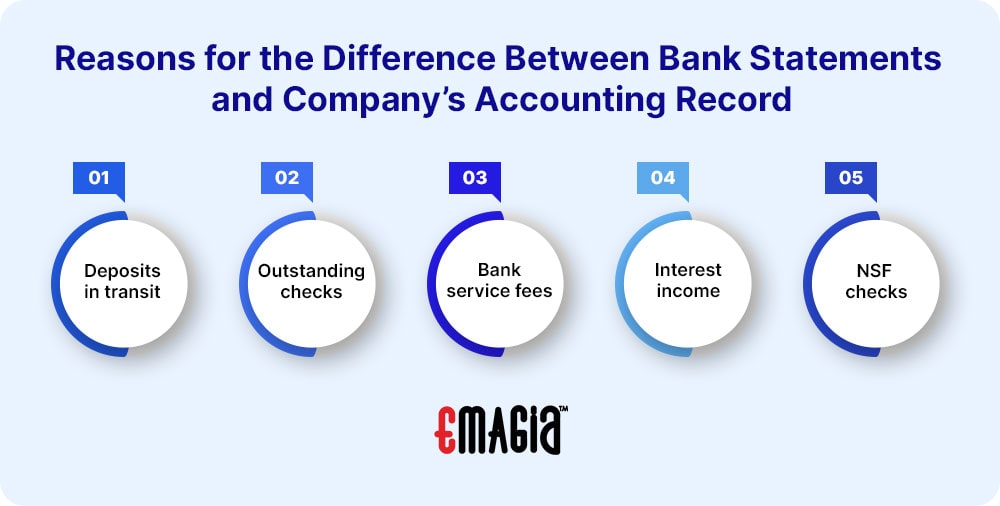

Reasons for the Difference Between Bank Statements and Company’s Accounting Record

When banks transfer companies a bank statement that contains the company’s start cash balance, transactions during the period, and ending cash balance, the bank’s ending cash balance and the company’s ending cash balance are nearly always different. Some reasons for these differences are:

- Deposits in transit: A business has to deposit a payment with their bank after collecting it. This must be done if the payment is in cash or check form. If a cash deposit is made, it takes till the next day for funds to appear in the business’s bank account. Deposits in transit can also occur from checks that are still in the office or that have been mailed.

- Outstanding checks: A check that a business has gotten but has not deposited in the bank yet. Another possibility is that it could be a business check that the recipient has not deposited yet.

- Bank service fees: Fees that are regarded with many types of bank services like account service and expedite payments. Usually, an exact amount is not shown until it is clear in the bank statements.

- Interest income: Like bank service fees, an exact amount is not shown until it is in the bank statement. This amount is usually recorded in the business’s books during bank reconciliation.

- Not sufficient funds (NSF) checks/ bounced checks: If a business wants to deposit a client’s check, however, does not have the right amount of money to do so, the transaction will be unsuccessful. When the check bounces, the payer as well as the recipient will have to pay a fee.

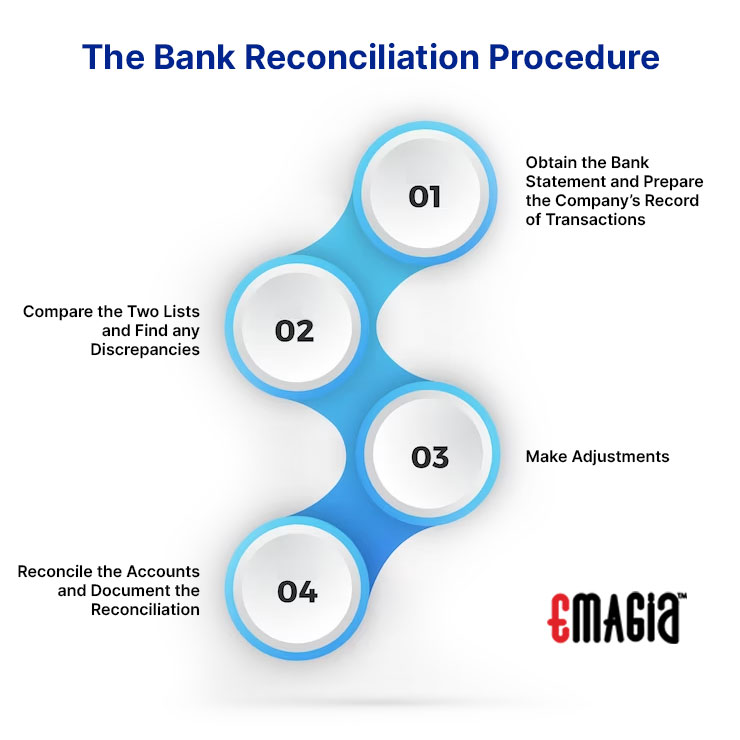

The Bank Reconciliation Procedure

Bank reconciliation is the process of comparing a company’s bank statement with its own accounting records to ensure that the two balances match. The following is a general procedure for bank reconciliation:

1. Obtain the Bank Statement and Prepare the Company’s Record of Transactions

You first need the list of transactions from the bank. This can be obtained from a bank statement or even having the bank deliver the information to the accounting software.

2. Compare the Two Lists and Find any Discrepancies

With both of these pieces of information, you can compare the deposits. When comparing the credit side of the bank statement with the debit side, you can compare the amount of each deposit that is recorded in the cashbook’s debit side of the bank column with that specific amount. Then, you can identify which items occur in both lists.

3. Make Adjustments

You can make any required adjustments to bank statements by adding any deposits, clearing any checks that are outstanding, and fixing any bank mistakes.

Reduce Lockbox Fees with Remittance Data Capture AI. Read eBook

4. Reconcile the Accounts and Document the Reconciliation

You can attach a note at the bottom of the book describing the discrepancies. You can also make a bank reconciliation statement that shows the specific reason for any discrepancy that may have occurred. The final statement depicts the bounced checks and their required information like the date, the exact amount, as well as payer.

Bank reconciliations find any errors in bank statements and give a very accurate depiction of the cash flow. A bank reconciliation should occur daily so that it is easier to sort out any problems immediately rather than sorting out a pile-up. It is a very effective process that corporations utilize to ensure that the balances that are recorded in their books align with the amount of cash they have in their banks. All in all, bank reconciliations are an excellent tool to handle cash flow by corporation owners.

FAQs about Bank Reconciliation

What are the Two Items You Need to Reconcile Your Checking Account?

Deposits in transit and outstanding checks.

What Do You Need to Do to Adjust Your Balance?

You need to primarily adjust the bank balance by adding any deposits, deducting any checks that may be outstanding, and identifying any bank errors during reconciliation.

Who Prepares a Bank Reconciliation Statement?

The account of a corporation or firm prepares the bank reconciliation statement.

Is Bank Reconciliation Simple?

Yes, it is very easy due to using accounting and free of errors.