Order to cash automation is the use of AI and workflow software to manage the full lifecycle from customer order to payment collection — covering credit evaluation, invoicing, collections, cash application, and dispute resolution in one connected system that reduces Days Sales Outstanding (DSO) by 15–30%.

Executive Summary for CFOs

- Reduce DSO by 15–30%

- Improve cash application rates to 85–95%

- Cut manual AR workload by 40–60%

- Increase collections productivity by 30–50%

- Strengthen working capital visibility across global entities

Order to Cash Automation at a Glance

O2C automation is closely related to accounts receivable automation, invoice-to-cash platforms, and working capital optimization technologies used in modern finance transformation initiatives.

| Concept | Description |

|---|---|

| Order to Cash (O2C) | The financial process that manages the lifecycle from customer order to payment collection. |

| O2C Automation | The use of AI, machine learning, and workflow technologies to automate credit, invoicing, collections, and cash application. |

| Accounts Receivable Automation | Technology used to streamline receivables operations and improve cash flow visibility. |

| Cash Application | The process of matching incoming payments to open invoices. |

| Collections Management | The strategies and systems used to recover outstanding receivables. |

| Deduction Management | The resolution of invoice disputes and payment deductions. |

What Is Order to Cash Automation?

Order to cash automation (O2C automation) refers to the use of artificial intelligence, machine learning, and workflow automation technologies to manage the entire financial lifecycle from customer order to cash receipt. The process includes credit evaluation, invoicing, accounts receivable management, collections, cash application, dispute resolution, and financial reporting.

O2C vs Quote-to-Cash vs Procure-to-Pay: What’s the Difference?

Three terms frequently appear together in enterprise finance discussions — Quote-to-Cash (Q2C), Order-to-Cash (O2C), and Procure-to-Pay (P2P). They are distinct processes that cover different parts of the revenue and procurement lifecycle.

| Process | Starts When | Ends When | Who It Serves |

|---|---|---|---|

| Quote-to-Cash (Q2C) | A prospect is quoted a price | Payment is collected and recognized | Sales + Finance — full revenue cycle |

| Order-to-Cash (O2C) | Customer places a confirmed order | Payment is received and posted | Finance + AR — post-sale revenue collection |

| Procure-to-Pay (P2P) | Company requests goods from a supplier | Supplier invoice is paid | Procurement + AP — outbound payments |

In short: Q2C is the broadest revenue process. O2C is a subset of Q2C that begins after the sale is closed. P2P is the mirror image — governing how money leaves your business to pay vendors, while O2C governs how money enters your business from customers. For most enterprise finance teams, O2C automation is the highest-ROI starting point because it directly impacts cash flow and working capital.

Executive Overview

Modern O2C automation platforms use artificial intelligence and workflow orchestration to streamline the entire receivables lifecycle — from order validation to invoice settlement and financial reconciliation.

For enterprises, AI-enabled receivables automation is essential to maintaining financial agility as business complexity increases. Finance leaders are moving away from manual methods toward a sophisticated O2C framework that optimizes cash velocity. For large organizations, the O2C function is a distributed financial system spanning multiple ERPs, regions, customer segments, shared services teams, and accounting structures.

This guide explains how enterprise finance leaders should structure, govern, and scale receivables automation to improve liquidity, accuracy, predictability, and financial control.

How Order to Cash Automation Works

O2C automation is the systematic use of integrated digital tools and automation software to manage the end-to-end receivables process — from order confirmation and invoicing to collections, cash application, dispute management, and reporting.

In practice, automation software replaces manual, spreadsheet-driven activities with connected solutions that improve revenue management, reduce operational risk, and provide enterprise-wide visibility across receivables. In large organizations, it represents an operating model rather than a single tool, connecting people, processes, systems, and data across geographies and business units.

Order to Cash Definition

The O2C meaning refers to the complete business process that begins when a customer places an order and ends when payment is received and recorded. The formal definition includes billing, accounts receivable, collections, cash application, deductions handling, and financial accounting — the entire lifecycle of a sale.

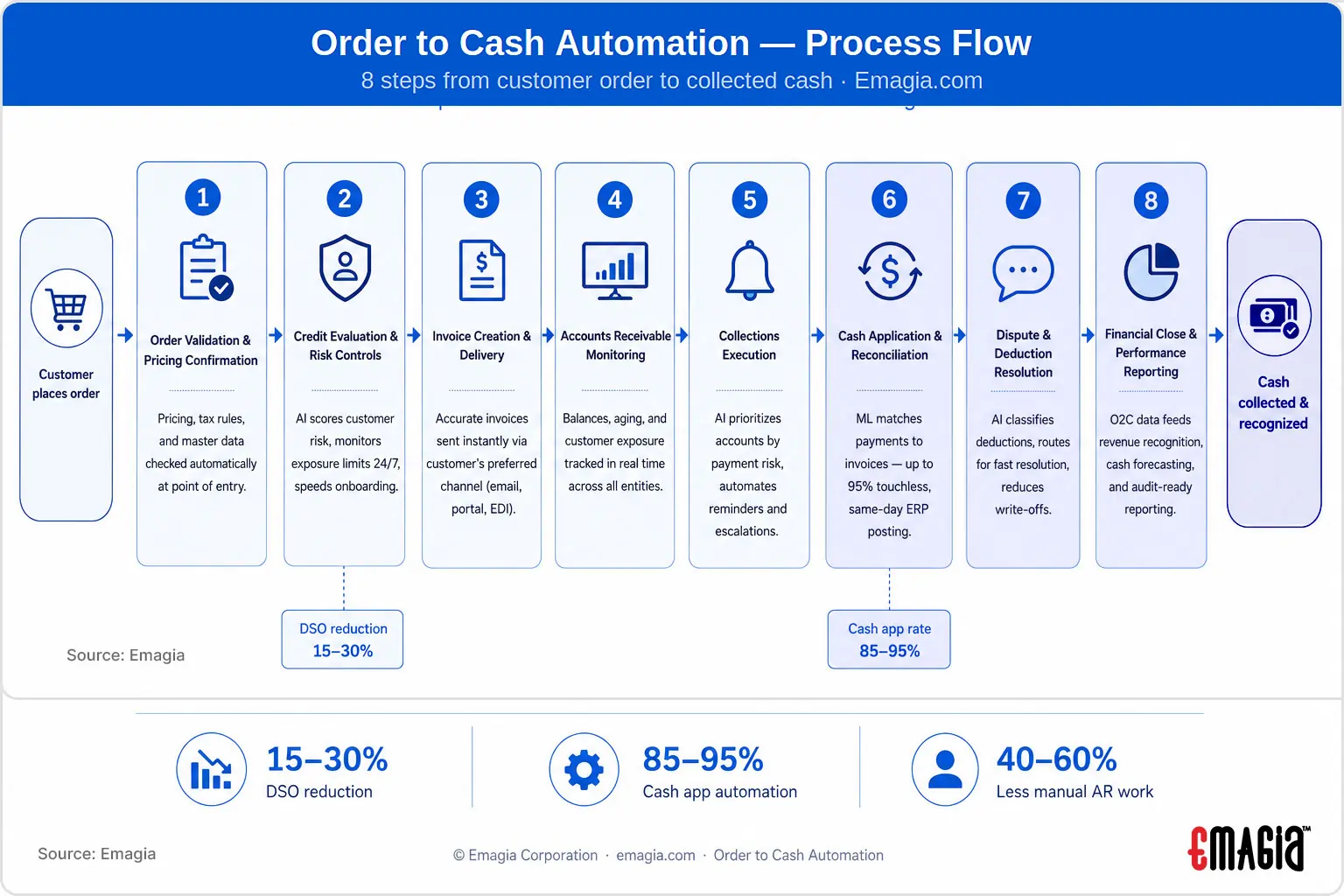

Order to Cash Process Flow

The O2C process consists of a sequence of financial activities that convert customer orders into collected revenue. Modern automation platforms connect these into an integrated digital workflow.

- Order validation and pricing confirmation

- Customer credit approval

- Invoice generation and delivery

- Accounts receivable monitoring

- Collections management

- Cash application and reconciliation

- Dispute and deduction resolution

- Financial reporting and revenue recognition

Why Enterprise O2C Automation Matters

Revenue is only realized when cash is collected accurately, on time, and with full financial control. Inefficiencies directly affect liquidity, forecast accuracy, audit readiness, and customer relationships. For CFOs, O2C performance directly impacts free cash flow, borrowing requirements, and shareholder value.

As transaction volumes grow and operating models become more complex, manual and fragmented approaches no longer provide the speed, resilience, or transparency required at scale.

Strategic Drivers for Enterprise Adoption

- Increasing transaction volumes without proportional headcount growth.

- Rising expectations for real-time cash visibility and forecasting.

- Greater regulatory scrutiny and audit requirements.

- Global shared services and multi-ERP operating models requiring standardized processes.

- Pressure to reduce DSO and eliminate revenue leakage.

Key O2C Metrics CFOs Should Track

Finance leaders evaluate the health of the AR cycle using several core performance metrics.

- Days Sales Outstanding (DSO)

- Cash application automation rate

- Collection effectiveness index (CEI)

- Average days delinquent (ADD)

- Dispute resolution cycle time

- Unapplied cash percentage

- Bad debt write-off rate

Enterprise O2C Operating Model

An enterprise operating model defines how people, processes, systems, data, and governance align across the full receivables lifecycle. Automation must support both centralized control and local execution.

Core Operating Model Components

- Standardized global process definitions.

- Configurable workflows by region or business unit.

- Unified receivables and cash visibility layer.

- Clear ownership and accountability by function.

- Embedded controls and auditability for compliance.

The Evolution of O2C: From Manual to Intelligent Systems

Historically, businesses viewed the AR cycle as reactive and siloed. Today, the O2C process is a proactive intelligence cycle. Modern platforms leverage AI-driven automation to predict payment behavior and reduce credit risk.

Step-by-Step O2C Process Explained

1. Order Confirmation and Data Validation

Order confirmation ensures customer orders comply with pricing agreements, contractual terms, tax rules, and master data standards. Automated validation reduces downstream disputes and billing errors by enforcing consistent data quality at the point of entry.

2. Credit Evaluation and Risk Controls

Credit management assesses customer risk using defined policies, historical payment behavior, and exposure limits. Organizations often use credit risk management software to automate credit scoring, monitor exposure, and reduce financial risk in the receivables lifecycle.

3. Invoice Creation and Delivery

Invoice generation translates fulfilled orders into accurate, compliant billing documents. This step is part of the broader billing-to-cash cycle, where timeliness and accuracy directly influence payment behavior. Automation ensures invoices are sent through the preferred customer channel instantly.

4. Accounts Receivable Monitoring

Accounts receivable teams track balances, aging, and customer exposure across entities. Modern O2C software provides real-time visibility for proactive collection prioritization.

5. Collections Execution

Collections processes include customer reminders, follow-ups, and escalations based on predefined strategies. Many enterprises deploy collections management software to automate customer outreach, prioritize accounts based on risk, and improve collector productivity.

6. Cash Application and Reconciliation

Cash application matches incoming payments to open invoices using remittance data, references, and algorithms. Modern enterprises rely on AI-powered cash application software to automate payment matching, reduce unapplied cash, and accelerate reconciliation across multiple ERP systems.

7. Dispute and Deduction Resolution

Dispute management governs the deduction process, ensuring discrepancies are identified and resolved quickly. Many enterprises implement deductions management software to streamline dispute tracking, root-cause analysis, and resolution workflows.

8. Financial Close and Performance Reporting

O2C data feeds revenue recognition, cash forecasting, and financial statements. Automation improves close speed, consistency, and audit confidence — bridging the gap between operations and financial accounting.

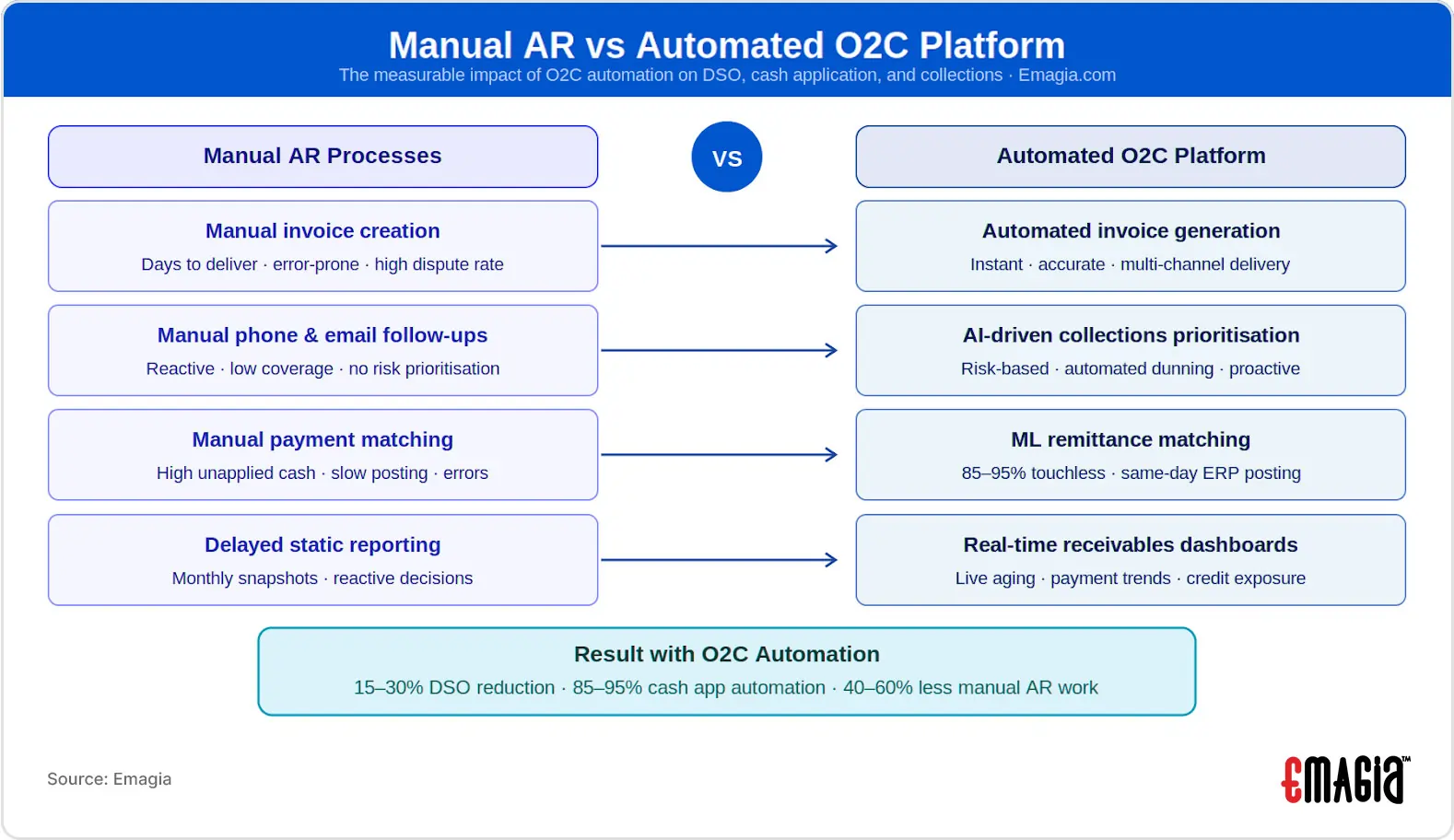

Manual vs Automated Receivables Processes

When enterprises assess manual processes against automated platforms, they consistently find that manual methods are the leading cause of revenue leakage — cash earned but never fully collected.

| Area | Manual AR Processes | Automated O2C Platforms |

|---|---|---|

| Invoice Processing | Manual creation and distribution | Automated digital invoice generation |

| Collections | Manual email and phone follow-ups | AI-driven collections prioritization |

| Cash Application | Manual invoice matching | Automated remittance matching using AI |

| Visibility | Delayed, static reporting | Real-time receivables analytics |

| Scalability | Linear headcount growth | Volume growth without proportional staffing |

| Control & Auditability | Limited traceability | Embedded controls and audit trails |

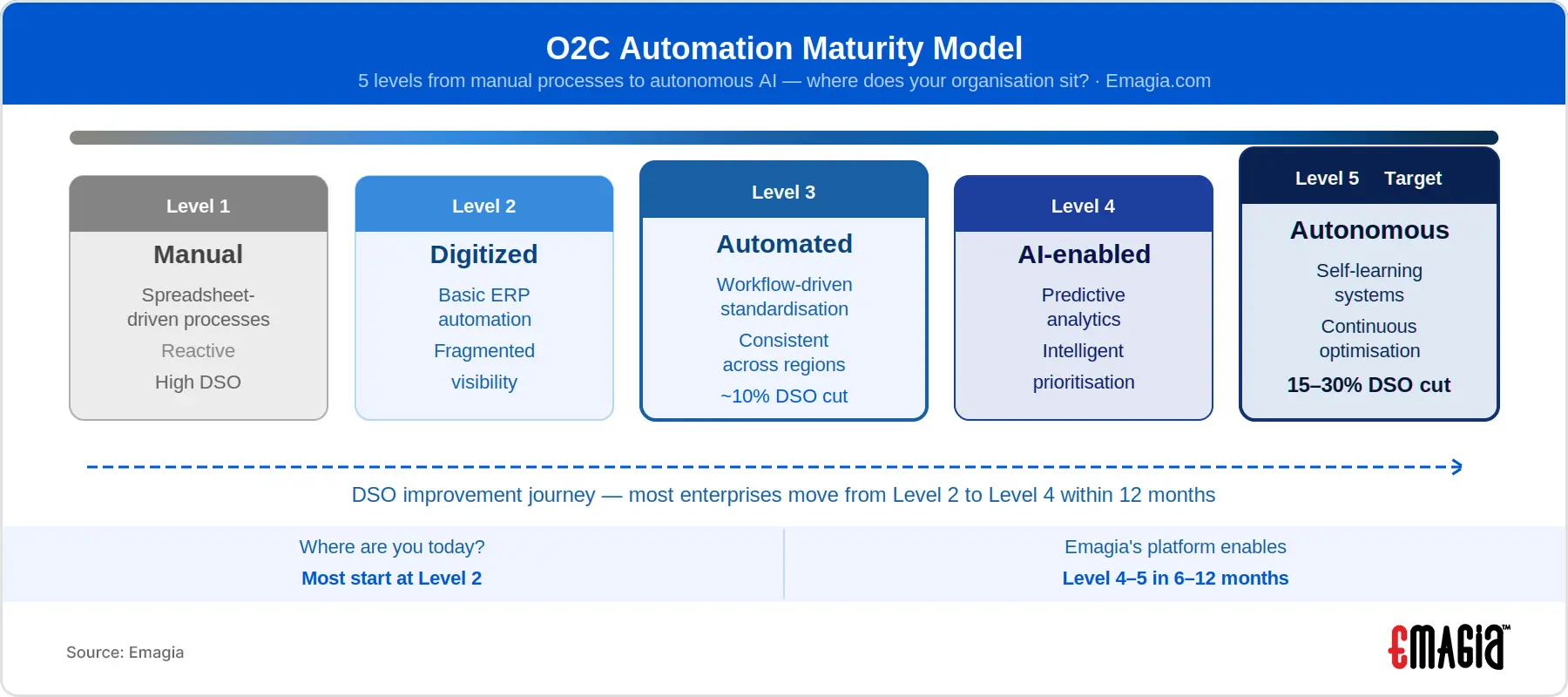

O2C Automation Maturity Model

- Level 1 – Manual: Spreadsheet-driven and reactive processes.

- Level 2 – Digitized: Basic ERP automation with fragmented visibility.

- Level 3 – Automated: Workflow-driven standardization across regions.

- Level 4 – AI-Enabled: Predictive analytics and intelligent prioritization.

- Level 5 – Autonomous: Self-learning systems that optimize cash flow continuously.

How AI Powers O2C Automation

Artificial intelligence enables finance organizations to transform receivables operations from reactive processing into predictive financial intelligence. Machine learning models analyze historical payment patterns, remittance behavior, and invoice characteristics to automate cash matching and prioritize collections strategies.

- Predictive payment risk scoring

- Automated remittance data extraction

- Machine learning cash matching

- AI-driven collections prioritization

- Automated deduction classification

These capabilities transform the AR function from a reactive back-office task into a predictive cash intelligence engine that continuously optimizes collections strategies, risk exposure, and liquidity outcomes.

Core Technologies Powering Enterprise O2C

- Workflow orchestration and rules engines for approvals, tasks, and escalations.

- Integration with multiple ERP, CRM, bank, and payment systems.

- Automated document generation for the billing-to-cash phase.

- Advanced analytics and intelligence layers for strategic insight.

Key Benefits of O2C Automation

O2C automation delivers measurable operational and financial benefits for enterprise finance organizations. By replacing manual receivables processes with AI-driven workflows, companies improve cash flow visibility, accelerate revenue realization, and strengthen liquidity performance.

- Faster cash flow and revenue realization. Automated invoicing, collections prioritization, and payment matching help organizations receive payments faster and reduce delays in the receivables cycle.

- Reduced Days Sales Outstanding (DSO). AI-powered collections strategies improve payment recovery rates and help finance teams focus on high-risk accounts — driving a 15–30% DSO reduction.

- Improved operational efficiency. Automation reduces manual data entry, spreadsheet management, and repetitive reconciliation tasks — cutting AR workload by 40–60%.

- Higher cash application accuracy. Intelligent remittance processing automatically matches payments to invoices, achieving 85–95% automation rates and reducing unapplied cash.

- Real-time receivables visibility. Modern platforms provide finance leaders with dashboards showing aging balances, payment behavior, and customer credit exposure.

- Improved compliance and financial control. Automated workflows create audit trails, enforce policies, and ensure consistent governance across global entities.

- Scalable finance operations. Enterprises manage increasing transaction volumes without proportional growth in finance headcount.

Working Capital Metrics Improved by O2C Automation

| Metric | Impact of O2C Automation |

|---|---|

| Days Sales Outstanding (DSO) | Reduced through faster invoicing and collections |

| Cash Conversion Cycle | Shortened through faster receivables processing |

| Unapplied Cash | Reduced through automated payment matching |

| Collections Efficiency | Improved through AI-driven prioritization |

How O2C Automation Improves Working Capital

Because accounts receivable represents a significant portion of working capital, improving the speed and accuracy of the receivables cycle has a direct impact on liquidity and financial performance.

- Accelerates invoice delivery. Automated invoicing ensures billing occurs immediately after order fulfillment, reducing delays that slow payment cycles.

- Reduces unapplied cash. Automated remittance matching ensures payments are reconciled quickly and accurately.

- Enhances receivables visibility. Real-time dashboards provide CFOs with a clear view of aging balances, payment trends, and exposure.

- Reduces operational inefficiencies. Automation eliminates manual processes that slow collections, reconciliation, and dispute resolution.

O2C Automation Industry Benchmarks

- Companies adopting O2C automation reduce DSO by up to 30%.

- AI-powered cash application achieves automation rates of 85–95%.

- Organizations reduce manual receivables work by 40–60%.

- Predictive collections strategies improve recovery rates by up to 25%.

O2C Automation by Industry

While O2C automation principles apply across all sectors, implementation priorities differ significantly by industry. Here is how leading organizations tailor their receivables automation approach by vertical.

O2C Automation for Manufacturing

Manufacturers face high deduction volumes, complex multi-location billing, and long payment cycles with distributors and retailers. O2C automation for manufacturing focuses on automating deduction classification, standardizing pricing across ERP instances, and accelerating cash application across high-volume transaction environments. The result is faster resolution of trade deductions, reduced write-offs, and improved DSO across global plant networks.

O2C Automation for Consumer Packaged Goods (CPG)

CPG companies deal with the highest deduction rates of any industry — promotional allowances, pricing disputes, and short-pays from major retailers are a daily reality. O2C automation for CPG addresses this through AI-powered deduction management that auto-classifies, routes, and resolves claims faster. Automated cash application with retailer-specific remittance handling ensures payments from major accounts are matched without manual intervention.

O2C Automation for Logistics and Transportation

Logistics companies operate on tight margins with high invoice volumes, fuel surcharge disputes, and complex multi-leg billing. O2C automation for logistics accelerates invoicing at point of delivery, automates proof-of-delivery matching, and ensures collections strategies account for the seasonal volatility of freight volumes. Real-time AR visibility helps finance teams manage cash flow during peak and off-peak periods.

O2C Automation for Technology and SaaS

Technology companies face unique challenges: subscription billing cycles, usage-based invoicing, and high-volume renewal collections. Automation ensures recurring invoices are generated accurately, payment reminders are personalized by customer tier, and cash application handles split payments across subscription and professional services lines without manual reconciliation.

Enterprise Use Cases for O2C Automation

- Global shared services centers managing multi-entity AR.

- Multi-ERP enterprises requiring unified receivables visibility.

- High-volume B2B environments with complex billing.

- Industries with high deductions (manufacturing, FMCG, distribution).

- Credit-intensive sectors requiring predictive risk control.

Who Uses O2C Automation?

- CFOs – Improve liquidity, reduce DSO, and strengthen financial visibility.

- Controllers – Enhance compliance, financial accuracy, and reconciliation efficiency.

- Accounts Receivable Teams – Automate collections, dispute resolution, and cash application.

- Shared Services Leaders – Standardize processes across global entities.

- Finance Transformation Leaders – Implement AI-driven automation strategies.

O2C Automation Best Practices for CFOs

Successful O2C transformation involves aligning technology, processes, governance, and change management to optimize performance and financial visibility.

- Standardize global processes before automating. Establish consistent workflows across regions and business units to ensure automation delivers scalable results.

- Integrate with ERP and financial systems. Effective platforms connect with ERP, CRM, and banking systems to create a unified receivables ecosystem.

- Leverage AI for predictive collections. Machine learning models can prioritize activities based on payment risk, invoice history, and customer behavior.

- Automate cash application and reconciliation. AI-powered matching engines significantly reduce unapplied cash and manual reconciliation work.

- Establish clear KPIs and performance dashboards. Track metrics such as DSO, collection effectiveness index (CEI), and dispute cycle times.

- Implement strong governance and compliance controls. Platforms should provide audit trails, policy enforcement, and financial transparency.

- Adopt a phased transformation approach. Implement automation modules gradually across credit, invoicing, collections, and cash application.

CFO Insight

Leading finance organizations increasingly treat O2C automation as a strategic working capital initiative rather than a back-office efficiency project. By combining AI-driven automation with strong governance and performance metrics, CFOs can significantly accelerate revenue realization and improve financial resilience.

Enterprise Challenges and Risk Considerations

Transitioning to an enterprise-grade receivables automation platform involves several common challenges:

- Process variability across global regions.

- Data quality and master data governance.

- Change management and user adoption.

- Integration complexity with legacy ERP systems.

Successful implementations address these through phased rollouts and strong executive sponsorship.

Key Features Enterprises Should Evaluate

When evaluating platforms, consider:

- Multi-ERP and multi-entity support.

- Configurable workflows and policies.

- AI-driven cash application and collections.

- Security, compliance, and audit controls.

Decision Framework for Selecting a Platform

| Evaluation Area | Key Considerations |

|---|---|

| Architecture | Cloud scalability and integration flexibility. |

| Enterprise Fit | Support for global, high-volume operations. |

| Automation Depth | AI and rule-based coverage across the full receivables lifecycle. |

| Governance | Controls, auditability, and compliance. |

| Total Cost of Ownership | Implementation, maintenance, and scalability costs. |

O2C Software and ERP Considerations

Many finance leaders adopt specialized platforms that integrate with existing ERP systems while providing advanced AI automation across receivables, collections, and cash application. Most large enterprises use a combination — relying on ERP systems for core transactional processing while layering specialized platforms for AI-driven receivables optimization. Emagia integrates natively with SAP, Oracle, NetSuite, and other leading ERP systems.

ROI of O2C Automation

Receivables automation platforms deliver measurable return on investment through improved liquidity, lower operating costs, and stronger financial governance.

- Accelerated cash inflows and improved free cash flow.

- Reduced manual workload and headcount dependency.

- Lower bad debt and credit exposure risk.

- Improved audit readiness and compliance control.

- Enhanced investor confidence through stronger working capital metrics.

Future Outlook

Enterprise O2C automation will focus on predictive cash forecasting, autonomous collections strategies, and deeper integration with upstream revenue processes. It will increasingly serve as a strategic intelligence layer for finance leaders — shifting the focus of transformation toward AI strategy rather than manual processing.

How Emagia Transforms the O2C Lifecycle

Emagia provides an AI-driven invoice-to-cash platform that bridges the gap between complex ERP data and actionable financial intelligence, designed to handle the scale and nuance of Global 1000 enterprises.

Emagia’s platform automates the cash application process with up to 95% touchless accuracy. By centralizing the receivables cycle, it enables finance teams to shift from data entry to data-driven decision making.

Key platform capabilities include:

- Seamless integration with multiple ERP systems including SAP, Oracle, and NetSuite.

- AI-driven cash application, collections, and analytics using the Gia digital assistant.

- Configurable workflows aligned to enterprise policies.

- Real-time visibility across global receivables.

- Scalable architecture supporting the highest transaction volumes.

Key Takeaways for Finance Leaders

- O2C automation accelerates revenue realization by eliminating manual receivables workflows.

- AI-driven cash application and collections significantly reduce Days Sales Outstanding.

- Modern platforms unify receivables data across ERP, banking, and payment systems.

- Predictive analytics allows finance teams to anticipate payment risk and optimize collections strategies.

- Automation enables global shared services teams to scale operations without proportional staffing growth.

Frequently Asked Questions About O2C Automation

What is AR automation?

AR automation uses AI and intelligent workflows to automate the full receivables lifecycle — from credit and invoicing through cash application and dispute resolution.

It enables enterprises to accelerate cash flow, reduce manual effort, and improve working capital visibility. While AR automation focuses on receivables management, O2C automation covers the broader lifecycle including order validation and financial reporting.

How does AR automation reduce DSO?

AR automation reduces DSO by 15–30% through faster invoicing, AI-driven collections prioritization, and automated cash application.

It does this by accelerating invoice delivery, prioritizing high-risk accounts using predictive analytics, automating payment matching, and resolving disputes faster. AI-driven prioritization ensures high-risk accounts receive proactive attention, improving payment velocity across the entire portfolio.

What processes are included in enterprise AR automation?

Enterprise O2C automation covers the complete receivables lifecycle — from order validation and credit to cash application and analytics.

- Order validation and pricing controls

- Credit risk assessment

- Invoice generation and delivery

- Accounts receivable monitoring

- Collections strategy execution

- Cash application and reconciliation

- Deduction and dispute management

- Reporting and receivables analytics

What KPIs improve with O2C automation?

Key improvements include 15–30% DSO reduction, 85–95% cash application automation, and 30–50% gains in collector productivity.

- 15–30% reduction in DSO

- 85–95% automated cash application rates

- 30–50% improvement in collector productivity

- Reduction in unapplied cash

- Faster dispute resolution cycles

- Improved cash forecasting accuracy

How does AI enhance O2C automation?

AI transforms O2C from reactive processing into proactive cash intelligence by predicting payment behavior and automating matching and prioritization.

Specifically, AI enhances O2C by predicting customer payment behavior, automatically matching remittances to invoices, classifying deductions using machine learning, prioritizing collections based on risk scoring, and improving forecast accuracy with predictive analytics.

What is the difference between O2C, Q2C, and P2P?

Q2C covers the full revenue cycle from quoting to payment. O2C is a subset starting after order placement. P2P is the mirror process managing outbound supplier payments.

Quote-to-Cash (Q2C) is the broadest process, encompassing quoting, contracting, and payment collection. Order-to-Cash (O2C) begins only after the order is confirmed and focuses on billing, AR, and cash collection. Procure-to-Pay (P2P) governs the purchasing side — how money leaves the business to pay vendors.

Can O2C automation integrate with multiple ERP systems?

Yes. Enterprise O2C platforms integrate with SAP, Oracle, NetSuite, and other ERP, CRM, and banking systems.

They create a unified receivables visibility layer across global entities while maintaining compliance and audit controls — solving one of the most common pain points for multi-ERP enterprises.

How long does implementation take?

Most enterprise deployments go live in phases, with initial modules launching within months and full transformation over 6–12 months.

Timelines vary based on complexity, ERP landscape, and geographic scope. Phased approaches consistently deliver better adoption and measurable ROI faster than big-bang implementations.

Is O2C automation suitable for global shared services centers?

Yes — O2C platforms are especially effective for shared services, standardizing workflows and scaling without proportional headcount growth.

They centralize receivables visibility, support multi-entity operations, and maintain governance across regions — making them ideal for organizations with complex global operating models.

What challenges should enterprises consider before implementing?

The most common challenges are inconsistent global processes, poor master data quality, change management resistance, and integration complexity.

- Inconsistent global process definitions

- Poor master data quality

- Change management resistance

- Integration complexity with legacy systems

- Governance and compliance requirements

What should CFOs look for in O2C automation software?

CFOs should prioritize multi-ERP support, AI-driven automation, real-time visibility, embedded compliance controls, and measurable ROI on DSO.

- Multi-ERP and multi-entity support

- AI-driven cash application and collections

- Real-time receivables visibility

- Embedded compliance and audit controls

- Scalability for high transaction volumes

- Measurable ROI impact on DSO and working capital

Quick Answers

What does O2C stand for in finance?

O2C stands for Order to Cash — the financial process that manages the lifecycle from customer order to payment collection.

What software automates order to cash?

O2C automation platforms integrate credit management, invoicing, collections, cash application, and receivables analytics into a unified finance system. Examples include Emagia, HighRadius, and similar AI-driven receivables platforms.

Why is order to cash important for CFOs?

The O2C cycle directly impacts working capital, cash flow predictability, revenue recognition accuracy, and financial risk management — making it one of the highest-ROI areas for finance transformation.

Is order to cash automation the same as AR automation?

Not exactly. O2C automation covers the entire revenue cycle from order to payment, while AR automation focuses specifically on receivables management. O2C is the broader discipline.

What industries benefit most from O2C automation?

Industries with complex billing and high receivables volumes — manufacturing, CPG, logistics, and technology — benefit most. Each has distinct deduction types, billing cycles, and ERP complexities that AI-powered O2C platforms are specifically designed to handle.

See How AI Transforms Order-to-Cash Operations

Leading global enterprises are adopting AI-powered platforms to automate credit, collections, cash application, and dispute resolution. Learn how Emagia’s autonomous O2C platform helps finance teams accelerate cash flow and improve working capital performance.